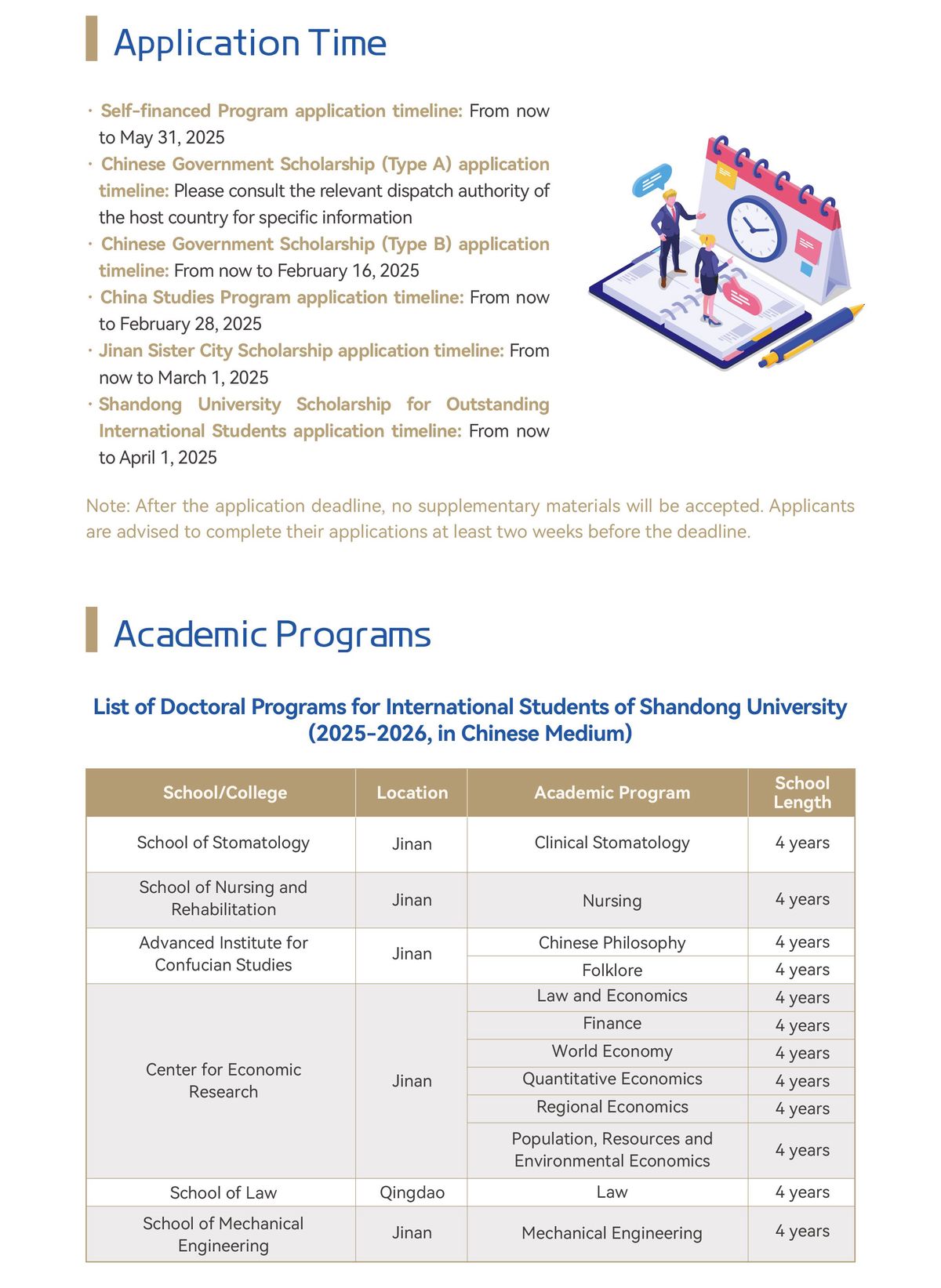

==============================================================

In the world of perpetual futures trading, understanding and managing risk is critical. One of the key risk metrics that professionals rely on is expected shortfall (ES), which measures the tail risk of a portfolio. This concept is essential for consultants in the perpetual futures market, as it helps assess the potential for extreme losses beyond the Value at Risk (VaR) threshold. In this comprehensive guide, we’ll delve into the concept of expected shortfall, explore how it can be applied in perpetual futures trading, and provide the necessary resources for consultants to optimize their risk management strategies.

What is Expected Shortfall?

Expected shortfall, also known as conditional VaR, measures the average loss that occurs beyond a certain quantile of the loss distribution. It provides a more comprehensive view of risk than Value at Risk (VaR), particularly when dealing with extreme events. While VaR tells you the maximum loss at a given confidence level (e.g., 95% or 99%), expected shortfall takes into account the severity of losses beyond that point, which is crucial for managing extreme risks in volatile markets like perpetual futures.

Why is Expected Shortfall Important for Perpetual Futures?

Perpetual futures are contracts that allow traders to speculate on the price of assets without an expiration date. These contracts are highly leveraged, which can magnify both gains and losses. As a result, expected shortfall is particularly valuable for assessing extreme risks that might not be captured by VaR. It helps traders and consultants gauge the potential for large losses, especially in situations where markets experience sudden, extreme movements.

In the context of perpetual futures, expected shortfall allows traders to:

- Measure the risk of large losses in highly volatile markets.

- Optimize portfolio allocations by better understanding tail risks.

- Adjust risk management techniques and strategies for improved capital preservation.

The Role of Expected Shortfall in Perpetual Futures Risk Management

In perpetual futures trading, risk management is crucial due to the high leverage involved. Traders often use expected shortfall as part of their broader risk management framework to determine the potential impact of tail events on their portfolios. Below are some common strategies consultants use to apply expected shortfall effectively:

1. Assessing Tail Risk in Volatile Markets

One of the most critical applications of expected shortfall is its ability to assess tail risk in markets prone to extreme price swings. Perpetual futures contracts are especially sensitive to these movements, given their nature of being open-ended and leveraged. By using expected shortfall, consultants can identify the risk of large, unforeseen losses and devise strategies to mitigate this risk, such as reducing position sizes or incorporating hedging strategies.

2. Optimizing Portfolio Allocations

Expected shortfall provides valuable insights into how different assets within a portfolio behave under stress. By considering the extreme losses in a portfolio, consultants can adjust asset allocations to reduce exposure to highly volatile instruments. This process helps create more resilient portfolios that are less prone to catastrophic losses, even during market crashes.

3. Scenario Analysis and Stress Testing

Consultants often use expected shortfall in combination with stress testing to simulate extreme market conditions. This helps them evaluate how a portfolio would perform in times of market crises, such as financial meltdowns or liquidity shocks. Understanding how portfolios behave under extreme conditions is key to creating more robust risk management strategies.

Key Resources for Perpetual Futures Consultants

To effectively manage risk using expected shortfall, perpetual futures consultants need access to a variety of resources. These resources include data, software tools, and analytical frameworks that allow them to calculate, optimize, and apply expected shortfall in their strategies.

1. Expected Shortfall Data for Perpetual Futures

Data is the foundation of any quantifiable risk management process. For perpetual futures, consultants need access to historical price data, volatility indicators, and liquidity metrics to calculate expected shortfall accurately. Some reliable sources for such data include:

- Cryptocurrency Exchanges: Platforms like Binance and FTX offer extensive historical data for perpetual futures contracts.

- Market Data Providers: Services like Bloomberg and Thomson Reuters provide real-time and historical data for perpetual futures on various assets.

- Blockchain Analytics Platforms: Tools like Glassnode and IntoTheBlock can help consultants assess on-chain data for crypto-based perpetual futures.

By combining price data with volatility indices, consultants can calculate the potential tail risks associated with a specific contract.

2. Expected Shortfall Calculation Tools

To calculate expected shortfall, consultants can use a variety of tools and software. These tools allow for efficient risk modeling and stress testing of portfolios. Some popular tools include:

- R and Python Libraries: R’s

PerformanceAnalyticspackage and Python’sRiskMetricslibrary provide comprehensive functions for risk analysis, including expected shortfall.

- MATLAB: A high-performance computing platform with advanced functions for risk management and financial modeling, including expected shortfall.

- Risk Management Platforms: Specialized platforms like MSCI RiskMetrics and Axioma provide tailored solutions for calculating expected shortfall in a wide range of asset classes.

These tools can automate the process of calculating and visualizing expected shortfall, allowing consultants to focus on more strategic aspects of portfolio management.

3. Expected Shortfall Models for Perpetual Futures Analysis

Several advanced models can be used to calculate expected shortfall in perpetual futures markets. Consultants can choose the model that best fits their needs based on the asset class and market conditions:

- Parametric Models: These models assume a normal distribution of returns and use parameters like the mean and standard deviation to calculate the expected shortfall.

- Non-Parametric Models: These models, including historical simulation and bootstrapping, do not assume any specific distribution, making them ideal for markets like perpetual futures where returns may not be normally distributed.

- Monte Carlo Simulation: Consultants can use Monte Carlo simulations to generate a large number of possible future market scenarios and calculate the expected shortfall for each one.

Practical Strategies for Using Expected Shortfall in Perpetual Futures

Consultants can use the following practical strategies to incorporate expected shortfall into their trading models:

1. VaR vs Expected Shortfall: A Comparative Approach

While both VaR and expected shortfall measure risk, they do so in different ways. Consultants often compare these two metrics to get a complete picture of the risk exposure in perpetual futures:

- VaR: Tells you the maximum loss at a specific confidence level (e.g., 99%).

- Expected Shortfall: Measures the average loss beyond that VaR threshold, providing a more accurate reflection of tail risk.

In many cases, expected shortfall is preferred over VaR because it accounts for the magnitude of extreme losses.

2. Hedging Using Expected Shortfall

Consultants can also use expected shortfall to design hedging strategies that minimize the impact of extreme market events. For example, implementing options or futures strategies that hedge against the worst-case scenarios identified by expected shortfall can help limit losses during periods of high volatility.

3. Incorporating Expected Shortfall into Portfolio Optimization

Expected shortfall can be used in portfolio optimization models to minimize risk while maximizing returns. By incorporating this metric, consultants can optimize position sizes and asset allocation, ensuring that the portfolio is resilient to extreme market movements.

FAQ (Frequently Asked Questions)

1. What is the difference between VaR and expected shortfall in perpetual futures?

VaR measures the maximum loss at a given confidence level, but it doesn’t account for the severity of losses beyond that point. Expected shortfall, on the other hand, measures the average loss in the tail of the distribution, providing a more comprehensive view of risk, especially in highly volatile markets like perpetual futures.

2. How can expected shortfall improve my perpetual futures model?

Expected shortfall can enhance your model by providing a better understanding of extreme risks. This allows you to adjust position sizes, optimize hedging strategies, and improve overall risk management, especially in periods of heightened volatility.

3. Where can I find expected shortfall data for perpetual futures?

You can access expected shortfall data from reliable sources like cryptocurrency exchanges (e.g., Binance or FTX), market data providers (e.g., Bloomberg, Reuters), or blockchain analytics platforms (e.g., Glassnode). These sources provide the historical price and volatility data needed for calculating expected shortfall.

Conclusion

Expected shortfall is an indispensable risk metric for perpetual futures consultants, offering a more comprehensive assessment of risk than traditional metrics like VaR. By understanding how to calculate, apply, and optimize expected shortfall, consultants can enhance their strategies and mitigate the potential for extreme losses in volatile markets. With the right tools, data, and models, consultants can successfully manage risk and develop robust trading strategies in the ever-changing world of perpetual futures.