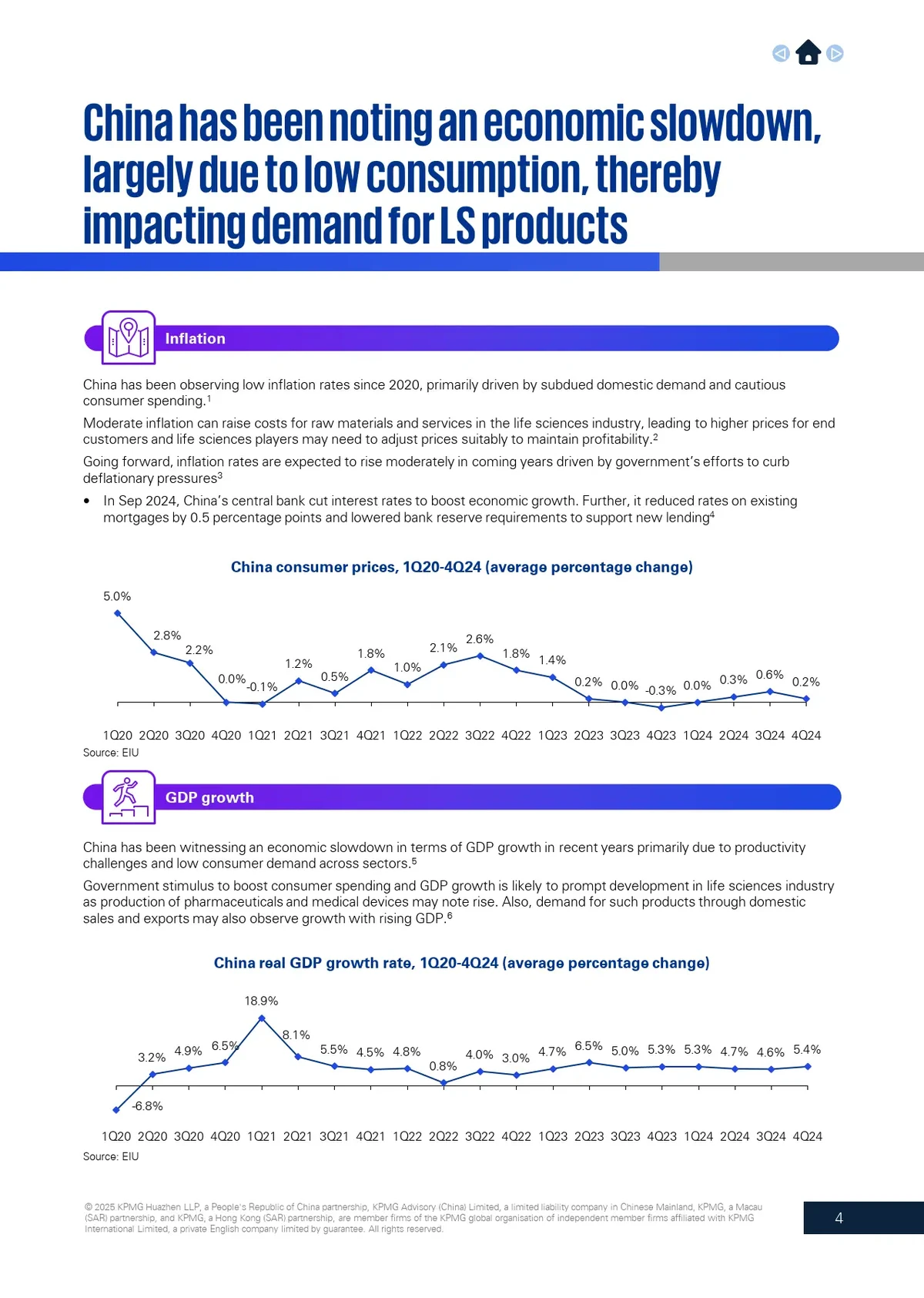

===========================================================

The Treynor ratio is a cornerstone of performance evaluation in finance, designed to measure returns relative to systematic risk. When applied to perpetual futures trading, it provides traders and institutional investors with a structured framework for understanding whether excess returns justify the market risk taken. This article explains how to interpret Treynor ratio results in perpetual futures, outlines different approaches, compares strategies, and highlights best practices based on real-world experience and the latest industry insights.

Understanding the Treynor Ratio in the Context of Perpetual Futures

What Is the Treynor Ratio?

The Treynor ratio, developed by Jack Treynor, is a risk-adjusted performance metric that calculates returns per unit of market (systematic) risk. Unlike the Sharpe ratio, which uses standard deviation, the Treynor ratio relies on beta to measure sensitivity to overall market movements.

Formula:

Treynor Ratio=Rp−RfβpTreynor\ Ratio = \frac{R_p - R_f}{\beta_p}Treynor Ratio=βpRp−Rf

- RpR_pRp: Portfolio or strategy return

- RfR_fRf: Risk-free rate

- βp\beta_pβp: Beta of the portfolio relative to the market

Why It Matters in Perpetual Futures

Perpetual futures, widely used in crypto, forex, and commodities, are highly leveraged instruments sensitive to both systematic and idiosyncratic risks. The Treynor ratio allows traders to:

- Compare strategies with different leverage levels.

- Assess whether alpha generation is real or just market exposure.

- Improve allocation and hedging decisions.

How to Interpret Treynor Ratio Results in Perpetual Futures

Positive vs. Negative Values

- Positive Treynor Ratio: Indicates excess returns for the risk taken. A higher value means better risk-adjusted performance.

- Negative Treynor Ratio: Suggests the strategy underperformed the risk-free rate, meaning traders took on market risk without adequate compensation.

Magnitude of the Ratio

- 0.1 – 0.3: Modest but consistent performance.

- 0.3 – 0.6: Strong efficiency in balancing return and market risk.

- 0.6+: Exceptional results, typically rare and sustainable only under disciplined strategies.

Industry Interpretation

- Retail Traders: Ratios above 0.3 are considered solid, given higher trading costs and slippage.

- Institutional Traders: Expect higher Treynor ratios due to advanced execution and hedging tools.

Methods for Applying and Interpreting Treynor Ratio

Method 1: Benchmark Comparison

Compare your perpetual futures strategy Treynor ratio against:

- A market index (e.g., BTC spot index for crypto perpetuals).

- A similar strategy (e.g., long-only vs. market-neutral).

Advantages:

- Simple, intuitive, and effective for strategy selection.

- Highlights whether a strategy adds value compared to passive exposure.

Disadvantages:

- Relies on accurate benchmark selection.

- May overlook idiosyncratic risks specific to perpetual futures (like funding rates).

Method 2: Multi-Period Analysis

Evaluate Treynor ratios across different timeframes (daily, weekly, quarterly).

Advantages:

- Identifies consistency in performance.

- Helps filter out noise from short-term volatility.

Disadvantages:

- Requires detailed historical data.

- May mask sudden risks if only averaged.

Comparison of the Two Methods

| Criteria | Benchmark Comparison | Multi-Period Analysis |

|---|---|---|

| Ease of Use | High | Moderate |

| Risk Insight | Medium | High |

| Best For | Beginners, retail | Institutional, advanced |

| Drawback | Benchmark bias | Data & analysis heavy |

Recommendation: Combine both methods—benchmarking for quick insights, multi-period analysis for deeper validation.

Real-World Insights: Treynor Ratio in Crypto Perpetuals

Impact of Funding Rates

Funding costs directly affect strategy returns. If ignored, Treynor ratios may overestimate true performance.

Volatility Regimes

In crypto markets, Treynor ratios can fluctuate drastically depending on bull vs. bear cycles. Interpreting ratios requires context.

Algorithmic Adjustments

Professional quant teams are increasingly integrating dynamic beta estimation into Treynor ratio analysis, accounting for time-varying market sensitivities.

Practical Applications and Best Practices

1. Strategy Evaluation

Use Treynor ratio to rank multiple perpetual futures strategies, identifying which ones provide true alpha vs. disguised beta exposure.

2. Portfolio Optimization

Integrate the ratio into portfolio allocation frameworks, favoring strategies with higher Treynor scores for capital efficiency.

3. Performance Monitoring

Track Treynor ratios over time to detect when a strategy loses edge, enabling timely adjustments.

Internal Link Integration

Before interpreting results, it is crucial to understand how to calculate Treynor ratio for perpetual futures accurately, ensuring beta estimation reflects the chosen benchmark. Additionally, traders must recognize why the Treynor ratio is important in perpetual futures, as it directly guides decisions on whether to scale positions or adjust leverage.

Visual Example of Treynor Ratio Interpretation

Interpreting Treynor ratios requires context: benchmark selection, volatility cycles, and funding rate effects.

Common Mistakes in Interpreting Treynor Ratios

- Ignoring Beta Accuracy – Using static beta can misrepresent risk, especially in volatile assets.

- Overlooking Funding Costs – Net returns must be used for correct evaluation.

- Comparing Across Inconsistent Benchmarks – Different reference indices distort insights.

- Assuming High Ratio Guarantees Sustainability – Outliers may indicate unsustainable strategies or excessive leverage.

FAQ: Treynor Ratio in Perpetual Futures

1. What is considered a “good” Treynor ratio in perpetual futures?

A ratio above 0.3 is generally considered good for retail traders, while institutional traders aim for higher ratios (>0.5). The “good” threshold depends on market conditions, execution quality, and leverage usage.

2. How is Treynor ratio different from Sharpe ratio in perpetual futures?

- Treynor Ratio: Measures performance relative to systematic risk (beta).

- Sharpe Ratio: Uses total volatility (standard deviation).

For perpetual futures, Treynor ratio is useful in identifying whether excess returns are truly market-driven or strategy-specific.

3. Can Treynor ratio be negative, and what does it mean?

Yes. A negative Treynor ratio means the strategy underperformed the risk-free rate relative to its market risk. It signals that traders would have been better off holding a risk-free asset than trading leveraged perpetuals.

Conclusion: Building Smarter Strategies with Treynor Ratio

Interpreting Treynor ratio results in perpetual futures is not just about reading a number—it’s about understanding context. Benchmark comparisons highlight relative performance, while multi-period analysis ensures consistency. Traders who integrate Treynor ratios into their strategy evaluation frameworks gain deeper insights into risk-adjusted efficiency and long-term sustainability.

The best approach combines accurate beta estimation, funding rate adjustments, and contextual analysis. By doing so, traders—whether retail or institutional—can turn the Treynor ratio into a powerful tool for navigating volatile perpetual futures markets.

Did this article help clarify Treynor ratio interpretation? Share it with fellow traders and drop your experiences in the comments—let’s discuss how Treynor analysis has influenced your trading decisions.