============================================================================

The Sharpe Ratio is a cornerstone metric in investment analysis, allowing investors to evaluate performance on a risk-adjusted basis. With markets growing increasingly complex, having a reliable Sharpe Ratio comparison tool for investors is vital for both retail and institutional participants. This article explores the importance of the Sharpe Ratio, demonstrates comparison strategies, highlights best tools, and provides actionable insights to optimize portfolio performance.

Understanding the Sharpe Ratio

What is the Sharpe Ratio?

The Sharpe Ratio measures the return of an investment relative to its risk, expressed as:

Sharpe Ratio=Rp−Rfσp\text{Sharpe Ratio} = \frac{R_p - R_f}{\sigma_p}Sharpe Ratio=σpRp−Rf

Where:

- RpR_pRp = Portfolio return

- RfR_fRf = Risk-free rate

- σp\sigma_pσp = Standard deviation of portfolio returns

Key Advantages:

- Standardizes returns relative to volatility

- Facilitates comparison across asset classes and trading strategies

- Helps identify risk-adjusted performance rather than just raw returns

Internal Link Integration: For traders exploring derivative markets, understanding how to calculate Sharpe Ratio in perpetual futures is crucial for evaluating risk-adjusted performance effectively.

Importance of Sharpe Ratio in Investment Analysis

- Risk Awareness: Distinguishes between high returns achieved through risk and genuine performance efficiency.

- Portfolio Optimization: Aids in selecting assets that contribute to optimal risk-adjusted returns.

- Performance Benchmarking: Compares multiple funds, ETFs, or trading strategies on a consistent basis.

Methods for Comparing Sharpe Ratios

1. Historical Data Analysis

Evaluating historical returns and volatility provides a baseline Sharpe Ratio. Investors can analyze multiple strategies over varying timeframes to determine which has delivered superior risk-adjusted performance.

Steps:

- Gather historical price or return data

- Calculate daily, weekly, or monthly returns

- Compute mean return, standard deviation, and Sharpe Ratio

- Compare across strategies or assets

Pros:

- Simple to implement

- Provides long-term insights

Cons:

- Backward-looking, may not reflect future market conditions

- Sensitive to extreme outliers

2. Monte Carlo Simulations

Monte Carlo techniques simulate multiple market scenarios to estimate potential Sharpe Ratios under diverse conditions. This approach considers variability and extreme events that may not appear in historical data.

Pros:

- Captures a range of possible outcomes

- Useful for stress testing portfolios

Cons:

- Requires computational resources

- Assumes model inputs are accurate

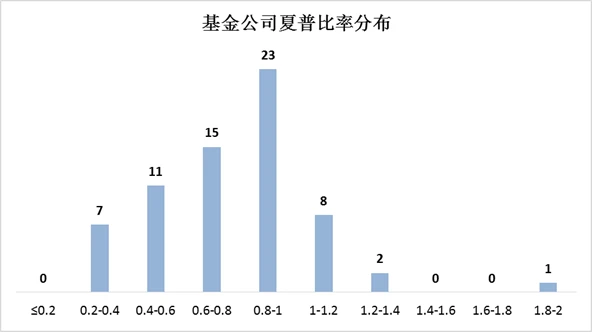

Example of Sharpe Ratio comparison across multiple assets using historical and simulated data.

Tools for Sharpe Ratio Comparison

1. Online Calculators and Platforms

Several platforms provide real-time Sharpe Ratio calculations and comparison capabilities:

- Portfolio management software with built-in risk metrics

- Online comparison tools that integrate multiple funds or ETFs

Internal Link Integration: Learn where to find Sharpe Ratio analysis tools online to access features such as automated calculations, historical benchmarks, and visual analytics.

2. Algorithmic Trading Platforms

Advanced platforms allow for Sharpe Ratio computation in trading strategies:

- Evaluate algorithmic trading models on a risk-adjusted basis

- Incorporate transaction costs and slippage into calculations

- Optimize parameters to improve Sharpe Ratios

Example Platforms:

- QuantConnect, MetaTrader, TradingView with scripting capabilities

Strategies to Improve Sharpe Ratio

1. Portfolio Diversification

Reducing unsystematic risk improves the Sharpe Ratio by lowering overall portfolio volatility without sacrificing returns.

Tactics:

- Mix equities, fixed income, commodities, and alternative assets

- Include hedged positions or inverse ETFs for downside protection

2. Active Risk Management

Use stop-loss, position sizing, and volatility targeting to control downside risk. A lower standard deviation of returns improves the Sharpe Ratio.

3. Leverage and Hedging Adjustments

- Moderate use of leverage can amplify returns but must be paired with hedging to prevent disproportionate risk

- Dynamic hedging strategies optimize risk-adjusted returns

Graph showing portfolio performance before and after Sharpe Ratio optimization using diversification and risk management techniques.

Practical Tips for Investors

Choosing the Right Comparison Tool

- Ensure it allows for multi-asset comparisons

- Provides real-time updates and historical benchmarks

- Integrates risk-free rate adjustments for accurate analysis

Avoiding Misinterpretation

- High Sharpe Ratio doesn’t guarantee consistent returns

- Consider the period and frequency of returns used in calculation

- Compare similar asset classes for meaningful insights

FAQ: Sharpe Ratio for Investors

1. Why use Sharpe Ratio for evaluating risks?

The Sharpe Ratio standardizes returns relative to volatility, allowing investors to discern whether higher returns are due to smart strategy or excessive risk-taking.

2. How does Sharpe Ratio compare with other metrics?

While metrics like Sortino Ratio focus on downside risk, the Sharpe Ratio considers total volatility. Combining multiple metrics provides a holistic risk-return assessment.

3. Where to apply Sharpe Ratio in trading strategies?

It’s useful in portfolio allocation, performance benchmarking, and algorithmic trading evaluation. Strategies with higher Sharpe Ratios are generally preferred for long-term risk-adjusted performance.

Conclusion

A Sharpe Ratio comparison tool for investors is indispensable for modern portfolio management. By leveraging historical data, simulation models, and advanced platforms, investors can identify strategies that optimize returns relative to risk. Combining this analysis with diversification, risk management, and algorithmic evaluation enhances overall investment efficiency.

Engage & Share: Apply Sharpe Ratio analysis to your portfolios, compare strategies, and share insights with fellow investors to foster informed, risk-aware decision-making.

Visualization of multiple investment strategies compared using Sharpe Ratio metrics.