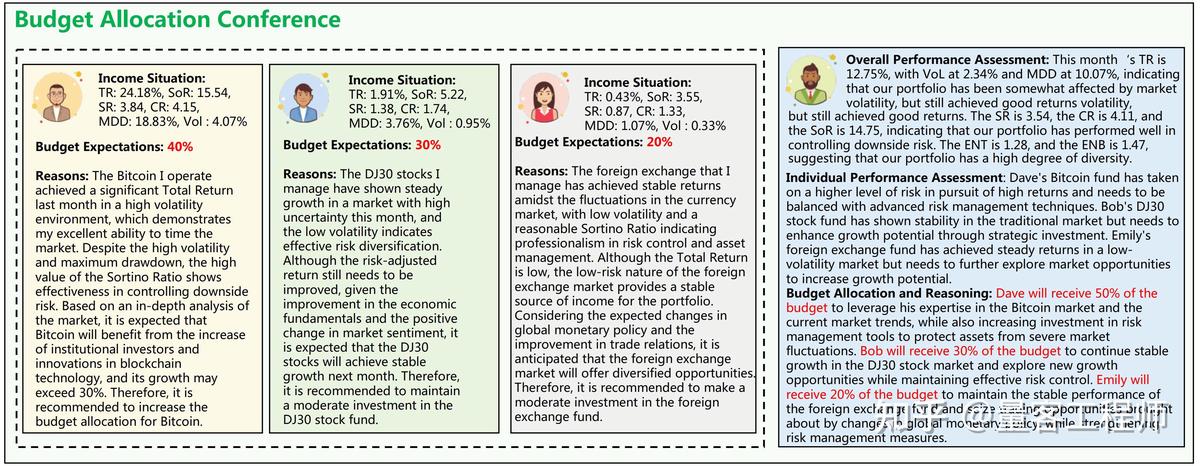

=======================================

Introduction

In today’s volatile financial landscape, minimizing default risk for hedge funds has become one of the most critical aspects of fund management. With hedge funds often engaging in leveraged trades, complex derivatives, and illiquid investments, the possibility of counterparty default can directly threaten portfolio stability and investor confidence. By adopting robust risk management frameworks, hedge funds can protect themselves from catastrophic losses while maintaining growth opportunities. This article provides a comprehensive guide to understanding, assessing, and mitigating default risk, drawing on real-world examples, expert practices, and the latest industry trends.

Understanding Default Risk in Hedge Funds

What is Default Risk?

Default risk refers to the possibility that a borrower, counterparty, or investment entity will fail to meet their financial obligations. For hedge funds, this risk can arise from corporate bonds, derivative contracts, repo agreements, or even prime brokers.

Why Default Risk is Critical for Hedge Funds

Unlike traditional investment funds, hedge funds often use leverage and derivatives to amplify returns. These strategies, while lucrative, magnify exposure to counterparties. As highlighted in discussions such as Why default risk matters in perpetual futures, default risk directly affects pricing, liquidity, and overall market confidence.

Types of Default Risk Faced by Hedge Funds

- Counterparty Risk: The chance that a derivatives counterparty fails to fulfill contractual obligations.

- Credit Risk: Exposure to issuers of bonds, structured products, or private debt instruments defaulting.

- Systemic Risk: Market-wide shocks leading to defaults across multiple institutions.

Strategies to Minimize Default Risk

Diversification of Counterparties

One effective method for minimizing default risk is diversifying exposure across multiple counterparties. Hedge funds relying heavily on a single prime broker or derivatives dealer may be overly exposed if that entity defaults. By distributing trading and clearing relationships, hedge funds can ensure continuity even in the event of a counterparty collapse.

Enhanced Due Diligence and Monitoring

Rigorous credit analysis of issuers and continuous monitoring of counterparties’ financial health is essential. Hedge funds can leverage data tools, such as where to find default risk data for perpetual futures, to track market signals, credit spreads, and liquidity conditions.

Hedge fund risk monitoring dashboard

Method 1: Collateralization and Margin Management

Description

Collateralization involves requiring counterparties to post high-quality collateral (e.g., cash, government securities) against their exposures. Dynamic margining ensures that collateral requirements adjust with market conditions.

Pros

- Provides a safety buffer in case of counterparty default.

- Encourages counterparties to maintain financial discipline.

Cons

- Can reduce liquidity if too much capital is tied up in collateral.

- Overreliance on collateral can lead to false security in extreme systemic events.

Method 2: Credit Derivatives and Hedging

Description

Hedge funds often use credit default swaps (CDS) or options to hedge against counterparty or issuer defaults. By purchasing protection, funds transfer part of the risk to other market participants.

Pros

- Provides direct insurance against default events.

- Allows funds to maintain risky positions while reducing downside risk.

Cons

- Hedging costs can erode returns.

- CDS liquidity may dry up during severe market stress, limiting protection.

Comparing the Two Methods

While both collateralization and hedging provide significant protection, the best practice is often a hybrid approach. Collateralization manages day-to-day counterparty risk, while credit derivatives provide targeted protection against systemic or issuer-specific events.

Default risk mitigation strategies comparison

Advanced Risk Management Approaches

Stress Testing and Scenario Analysis

Hedge funds increasingly rely on stress testing to simulate extreme events, such as the 2008 financial crisis or sudden counterparty defaults. These tests allow managers to identify vulnerabilities and preemptively adjust positions.

Central Clearing and Regulatory Support

The post-2008 reforms introduced central clearing for standardized derivatives, which reduces bilateral counterparty exposure. Hedge funds participating in cleared markets enjoy greater transparency and reduced systemic risk.

Technology and Real-Time Analytics

Advanced analytics and machine learning models now help predict credit deterioration before defaults occur. These tools can track signals like credit spreads, trading volumes, and liquidity shifts in real time.

Practical Recommendations

- Adopt a multi-layered approach, combining collateralization, diversification, and hedging.

- Regularly perform stress tests under both historical and hypothetical scenarios.

- Use technology-driven solutions for real-time monitoring of counterparties.

- Educate portfolio managers and traders on default risk awareness, ensuring consistent risk discipline across the firm.

Frequently Asked Questions (FAQ)

1. What is the most effective way to minimize default risk in hedge funds?

The most effective method is combining collateralization with credit hedging, supported by ongoing due diligence. While collateral protects against immediate shortfalls, hedging offers coverage against systemic shocks. Together, they create a balanced and resilient framework.

2. How does default risk impact hedge fund performance?

Default risk can significantly reduce returns if not managed properly. Defaults lead to losses in capital, liquidity squeezes, and reputational damage. On the other hand, effective risk management strategies allow funds to take calculated risks without jeopardizing long-term performance.

3. Can small hedge funds manage default risk as effectively as large ones?

Yes, but small funds must rely more on outsourced services such as third-party credit analysis tools, central clearing platforms, and managed service providers. By leveraging industry-standard solutions, smaller funds can achieve comparable protection without building extensive in-house risk teams.

Conclusion

Minimizing default risk for hedge funds is not just about compliance—it is about survival and long-term success. By diversifying counterparties, collateralizing exposures, and using hedging instruments, hedge funds can effectively mitigate risks while pursuing higher returns. As financial markets evolve, incorporating advanced analytics and stress testing will be critical for staying ahead of potential shocks.

We encourage readers to share their perspectives: How does your firm manage default risk? Comment below, engage with peers, and share this article with your network to promote smarter, safer investing practices.

Would you like me to also prepare a short infographic version of this article (under 500 words + visuals) that you can use for quick social media sharing?